Market Timing vs. Peace of Mind

Should I wait to invest in the stock market?

March 21, 2025

I recently received the following question from a newsletter subscriber:

"We have about $25k coming in between a solar rebate and my bonus. Given the crazy ups and downs politically lately, should we put it in savings (3.7% APY) and gradually invest in the market over time, or put it all into the market right away? We're concerned about investing it all at once and then facing a huge market decline."

This is such a great question because it gets at something many of us struggle with — the desire to perfectly time our investments. But here’s something important to keep in mind when it comes to investing: Nobody knows what's going to happen.

So instead of trying to predict the unpredictable, let's focus on a better approach:

Time Horizon Buckets

The most reliable investment decision framework? Determine when you'll need the money:

Under 5 years: Keep your money in that high-yield savings account.

5-10 years: Split between stocks and high-yielding cash or bonds.

10+ years: Consider putting it all in the stock market (assuming you have your emergency cash buffer).

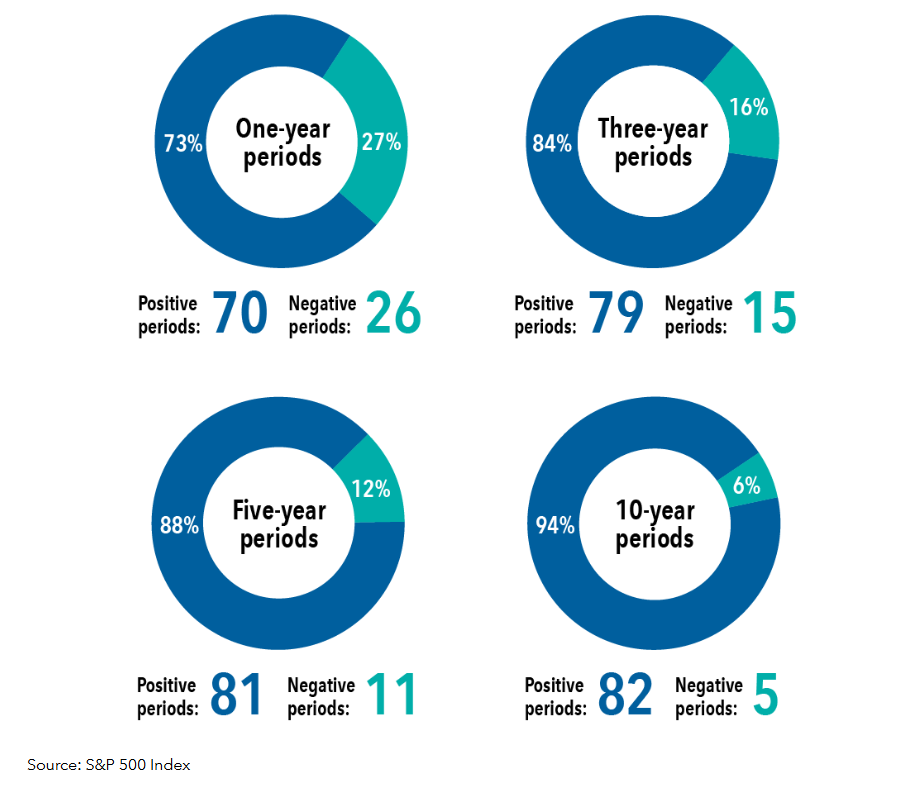

The following image from respected fund manager, Capital Group, illustrates why a longer time horizon can reduce the risk of owning stocks:

This "Time Horizon Buckets" approach is an easy way to take the guesswork out of where to put your money.

The Truth About Dollar Cost Averaging

Many investors assume gradually investing over time (dollar cost averaging) is safer. But research shows it offers more psychological comfort than mathematical benefit — and that comfort typically comes at the expense of your returns.

Consider this: the stock market has historically risen in over 70% of calendar years. When you gradually invest, you're essentially betting against these favorable odds.

Understanding Market Drops

The S&P 500 is currently in pullback territory (roughly 8% down from its previous high mark). This could develop into a sustained correction, which is worth understanding so you can manage your response.

Here are the different types of market declines you'll encounter as an investor:

Pullback: 5-10% drop (happens multiple times per year)

Correction: 10-20% drop (happens every couple years)

Bear Market: 20%+ drop (happens every 3-4 years)

Corrections are short, sharp drops typically driven by headlines rather than material problems. They're particularly dangerous because they can frighten you out of the market — right before an equally strong recovery. Missing these recoveries can severely impact your long-term returns.

Bear markets typically happen during investor euphoria (not what we're seeing now) or alongside unpredictable catastrophic events (like the COVID-19 pandemic). Having a solid plan that accounts for these inevitable events puts you ahead of investors who try unsuccessfully to predict them.

While there’s no way to know how the current downturn will materialize, in my opinion, it looks very much like the correction that I described above.

What This Means in Real Terms

True financial freedom isn't about maximizing every dollar. It's about having a plan that lets you live well regardless of market conditions.

When you're constantly trying to time the market perfectly, you create unnecessary stress. You might find yourself checking accounts too frequently and making emotional decisions that hurt your long-term wealth.

One of my clients put it perfectly in an email recently: "The best thing to come out of this? I’m confident now to disconnect from my phone and be more present with my kids. That's what financial planning truly does for us."

This is exactly what affordable freedom looks like — the confidence to focus on what truly matters in your life!

The Smarter Approach

The current market has already priced in known fears about policy changes. While some unforeseen event could certainly impact markets negatively, history suggests things often turn out better than feared.

The real risk for your portfolio isn't short-term volatility. It's missing the market's upside. Historical data consistently shows that being out of the market during key recovery periods is far more detrimental to your long-term returns than enduring inevitable drawdowns.

Your best strategy? Stay invested according to your time horizon and tune out the day-to-day noise.